3 – Tax and National Insurance (2026-27)

Last Updated on 7 April 2026

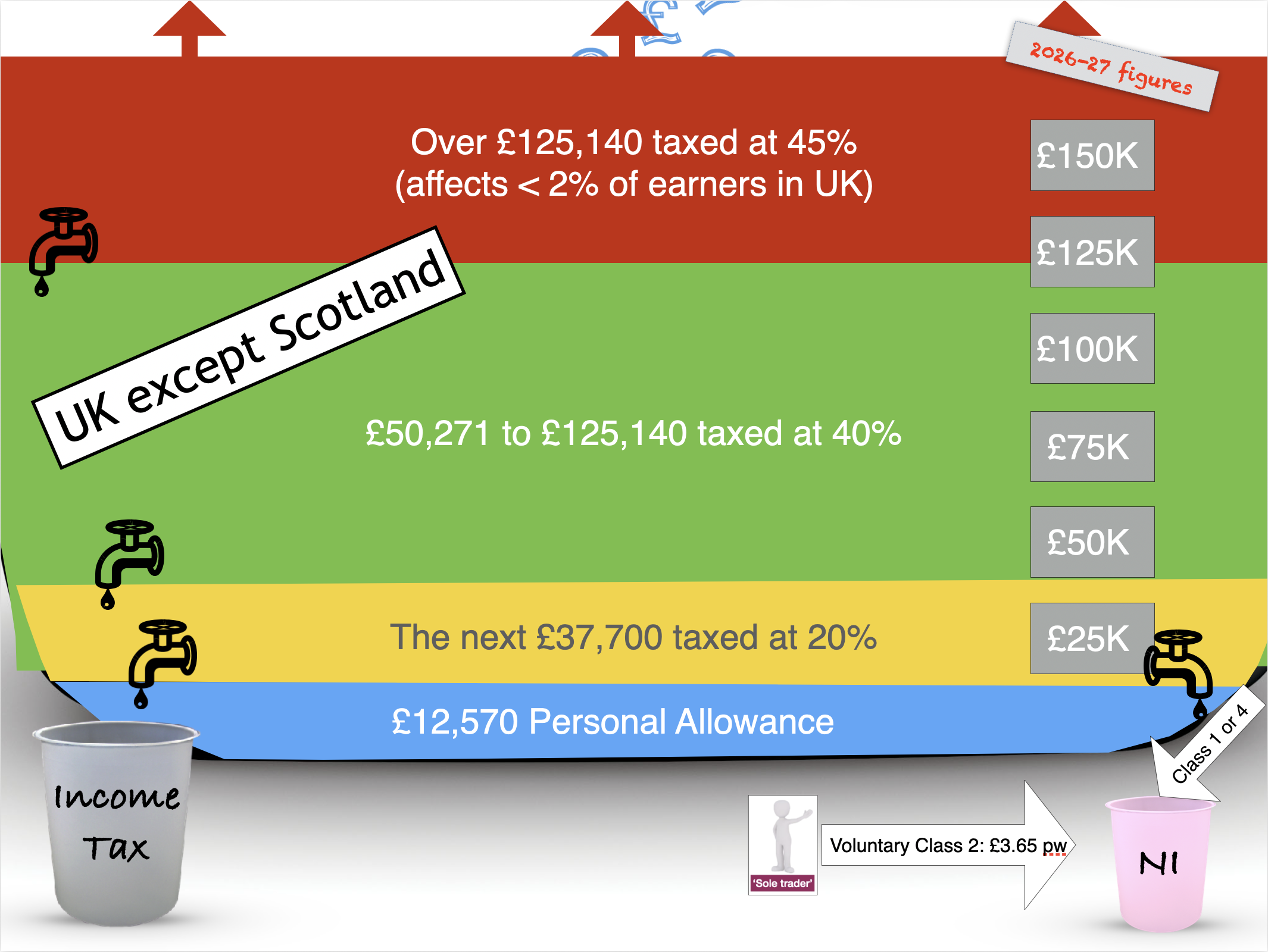

Do you live in Scotland? There’s a different help sheet for you!

See Scottish Tax and National Insurance help sheet >

National Insurance

Employees and company directors pay their NI via the company PAYE system. This is Class 1 National Insurance and is a percentage of the salary, normally 8% (2026-27).

National Insurance for Sole Traders (self-employed):

Sole traders pay two types of National Insurance:

- Voluntary Class 2 – £3.50 per week in 2025-26, £3.65 per week in 2026-2027. This is based on how many weeks of the previous tax year you were registered as a sole trader, not whether you had any income.

- Class 4 – 6% of profits (from the self-employed business) 2025-26 between £12,570-£50,270 (2% on taxable profits above £50,270)

Class 2 and Class 4 NICs are both taken through the tax return system at the end of the tax year.

Having a National Insurance record is important as it can entitle you to:

- Employment & Support Allowance (if sick)

- Maternity allowance

- Bereavements benefits (if you lose your spouse/civil partner)

- State pension

It’s not compulsory for sole traders to pay Class 2 NI. If your profits are at or above the Small Profits Threshold, (£6,845 per year in 2025-26; £7,105 per year in 2026-27) your NI record is credited automatically.

But if your profits are less than that threshold you can pay Class 2 voluntarily.

This can be useful for sole traders with low profits who are not making any NI contributions under PAYE elsewhere. It’s offered as a cheaper way for low-earning sole traders to add to their NI record.

You get a ‘credit’ to your NI record between the small profits threshold and £12,570. You don’t pay anything, but your NI record is ticked as if you have.

Above profits of £12,570 sole traders will pay Class 4 NI, which is 6% of profits (2026-27).

Making Voluntary Contributions (Class 3)

Class 3 are voluntary contributions, used to fill gaps and keep a record if you’re overseas or not working. The rate was £17.75 per week for 2025-26, £18.40 per week for 2026-27.

You can only go back up to 6 years to fill gaps. Read more here:

https://www.gov.uk/voluntary-national-insurance-contributions/deadlines >

Note: You are allowed to be both self-employed and employed at the same time, but be careful that you are not overpaying National Insurance contributions, as your employer pays your Class 1 NICs through the PAYE system.

In some circumstances you can get a refund on NI contributions:

https://www.gov.uk/claim-national-insurance-refund >

You normally stop paying National Insurance when you reach ‘state pension age’.

Read more on gov.uk about this here >

Tax

Sole traders will pay income tax on the business’s profits, after you’ve taken into account allowable business expenses, pension contributions, capital & personal allowances.

Some key dates for sole traders (and other income tax payers)

- The income tax year runs 6th April to 5th April

- 31 January – deadline for getting information to HMRC about the previous tax year’s income and expenditure.

Also the deadline for paying tax owing from the previous year(s) AND half the forecast amount owing for the current tax year. (This is called ‘payment on account’. See my blog entry explaining what it is >) - 31 July – deadline for any outstanding income tax not paid by the previous January.

It can take a couple of weeks to get your Government Gateway log in. So don’t leave it to January!

NB: Tax reporting is going digital for Sole Traders and landlords. See help sheet 4.

Limited Companies

Must register with HMRC for Corporation Tax and PAYE. Must use PAYE for directors and other employees. (Partnerships and sole traders must also operate PAYE system if they are directly employing anyone else.)

Corporation Tax is 19% for limited companies with profits less than £50K (2026-27). For companies with profits more than £250,000 the rate is 25%. There’s a sliding scale between £50K and £250K.

Dividend taxes:

Many Limited Company freelancers take some of their income as ‘dividends’. These are profits taken out of the business and distributed to the owners/shareholders.

From April 2026 there is a 2% increase to the basic and higher rates of the tax on dividend income. They are 10.75% and 35.75% respectively. The additional rate remains unchanged at 39.35%.

Find out more:

National Insurance Helpline – 0300 200 3500 (Weekdays only, 8am-5pm) www.gov.uk/personal-tax/national-insurance

www.gov.uk/claim-national-insurance-refund – if you think you’re owed some NI back

Income Tax Helpline – 0300 200 3300 (Weekdays 8am-6pm) | See full list of ways to contact HMRC

www.gov.uk/browse/tax

Help notes for filling in a tax return (gov.uk) >

www.gov.uk/understand-self-assessment-bill > – explains ‘payment on account’ too

www.hmrc.gov.uk/rates – pretty straightforward list of tax rates and thresholds

www.taxationweb.co.uk/ | www.freelanceuk.com/ – support for creative freelancers

www.litrg.org.uk – Low Incomes Tax Reform Group – charity with very good site

Unions will normally give advice to their members about tax status.

Useful HMRC (tax office) numbers for production freelancers:

– Freelance status,‘Lorimer Letters’/LP10 – 0300 123 2326 (option 1)

– IR35 enquiries – 0300 123 2326 (option 2)

Note: Income tax rates and thresholds for Scottish residents are different. (See separate help sheet >)

Posted on 29 January 2020